Introduction

Please reference [RFC] How to Increase [Liquidity for the HOP Token]

Over the past several weeks, there has been an on-going conversation around deepening liquidity for the HOP token, which plays an important role in governance and incentivizing deposits into the protocol’s cross-chain pools. I posted a Snapshot vote, which may have been premature as the Request for Comment post was only ~ a week old. 611 users joined the vote with a vast majority of the voting power choosing to not immediately move forward. The loudest criticisms were that the RFC was not posted long enough and the proposal was not detailed enough to be truly put to vote.

It is worth noting that many community members agreed with the underlying sentiment of the proposal, including many of those that voted “No Change.” There were hundreds of voters scattered across each of the multiple choice voting answers and dozens of community members who weighed in on the forum Temperature Check. I apologize for potentially rushing the first proposal through the process, however, I attempted to follow the recommendations put forth in a previous forum post and have not received exact feedback on what violations may have taken place.

After many discussions with the community and feedback from the community call and Discord discussions, it came to my attention that sufficient liquidity for HOP could be established through a longer-term / partnership focused strategy with the creation of a rETH / HOP pool on Arbitrum or Optimism. In a conversation with Rocketpool representatives, @dybsy found that the Rocketpool DAO would be willing to provide 100-200 RPL in co-incentives to a rETH / HOP pool to kickstart utility of rETH on Arbitrum or Optimism.

The purpose of this proposal is to continue the discussion around ways to improve DEX liquidity of the HOP token, as discussed in the previous RFC, while adding greater context to the specific technical, monetary, and time requirements each solution would mandate.

Problem Statement

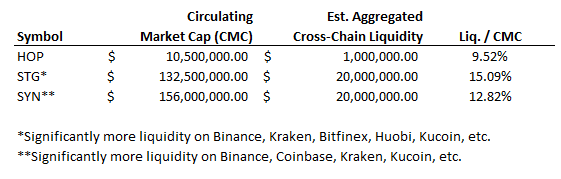

The HOP token is extremely illiquid in its current state, with liquidity fragmented across Optimism, Arbitrum, Polygon and Ethereum mainnet. To make matters worse, this liquidity is scattered across several different DEX’s, so that even whilst using a DEX aggregator, liquidity is still too thin to buy or sell without experiencing dangerously high slippage and commonplace sandwich attacks. As of April 12, buying 1 ETH worth of HOP via the DeFiLlama DEX Aggregator would result in 2.33% of price slippage. This creates a number of problems as outlined in the following section.

Logic & Benefits of Increasing Liquidity

HOP’s illiquidity can negatively impact the growth of the protocol and the community in several ways, including:

-

Prospective (and existing) community members becoming more hesitant to join the DAO, participate in governance matters, and/or contribute time and resources to the protocol once realizing they would take upwards of a 5% haircut (or being sandwiched attacked) just to make an initial investment. This effectively serves as a tax on new contributors and may prevent more experienced individuals from joining the community. Greater liquidity would incentivize more participation from a wider demographic of crypto native participants. Although holding HOP is not necessarily a prerequisite to participating in the community, it can be used as a tool to align economic incentives between contributors, delegates, delegators, liquidity providers, the core team, and all other stakeholders. The HOP token’s stability and transactability can ultimately reflect favorably or unfavorably on the protocol itself, whether or not it is integral to performing the protocol’s core functions.

-

HOP is primarily used as an incentive token for the protocol’s bridge pools and plays an instrumental role in ensuring that a sufficient amount of cross-chain liquidity exists for transacting users. LPs are rewarded with HOP for performing this critical function (2.2M HOP per month). Those participating in providing liquidity to the bridge often sell some or all of their HOP rewards, as a result of its lack of value proposition and poor liquidity. This further accelerates the liquidity crunch on DEXs, as it turns into a race to be the first one out the door. It would be in the best interest of all stakeholders if the price of HOP is not drastically impacted from continuous selling pressure from bridge LPs. It is also worth mentioning that there is not an infinite supply of HOP tokens. There will come a time where either HOP bridge LP emissions must stop entirely or be dramatically reduced. To provide the same level of economic utility to LPs while meeting the significant increase in transaction/user demand that we all hope to achieve, will require HOP to have a standalone value proposition allowing for such a reduction in supply emissions (while maintaining the same or greater dollar value). However, before that can even be discussed, sufficient liquidity must be available for purchasers.

Key Assumptions

The Hop treasury currently holds 826K OP (~$2M) and 1.67M ARB (~$2.5M). If 10% of these treasury assets were redirected to HOP/rETH liquidity providers, alongside 200 RPL over the next 12 months, the annualized yield would be upwards of 52.9% at the current level of liquidity ($850k). While it’s difficult to estimate the precise impact on notional liquidity added from this rewards program, it would likely be material.

As the Hop bridge is likely to add support for rETH in the near future, it makes sense to increase the utility of the token across other networks. This incentivized liquidity pool could easily drive rETH bridge volume and recoup some of the lost treasury emissions via bridging fees.

Other popular crypto protocols use several different tools to increase liquidity depth for their native token, including: inflationary token emissions, working with external market making firms or “bribing” DEX governance tokens: CRV, VELO, etc.

To provide a few examples of protocols that invest in increasing their native token’s liquidity: two of Hop’s largest competitors, Synapse (SYN) & Stargate (STG), bribe via Hidden Hand to direct emissions to their pools.

Potential Risks

Moving forward with an incentivized rETH / HOP pool runs the risk of further fractionalizing HOP liquidity, as rETH will be a newly integrated asset to layer 2 networks. While there are multiple benefits (Capital efficiency, partnership, driving bridge volume) to partnering with Rocketpool on this endeavor, it is possible that we may be too early in adopting rETH as the base pairing on a layer 2. If we were to complement RPL emissions by distributing OP and/or ARB incentive rewards from the DAO treasury, it will also reduce the number of different ways these tokens can be spent to grow the protocol/DAO.

It is also valuable to consider potential downsides and have alternative options for community members that disagree with this proposal, therefore I have again included a few options to consider as alternatives below.

Potential Paths Forward

These are by no means finalized and are just meant to exist as examples for potential solutions. It would be great to get community engagement and try to narrow down 1 to 2 solutions before moving forward with an official vote.

- Incentivized HOP / rETH pool on Camelot or another Arbitrum DEX

- Provides utility for rETH on L2 & strengthens Rocketpool partnership

- Stronger capital efficiency as the LP gets exposure to staking rewards

- Will likely receive co-incentives in RPL - which is also available on Arbitrum

- Incentivized HOP / ETH pools on Arbitrum & Optimism

- Use ARB, OP or HOP emissions to concentrate liquidity on a smaller number of DEXs within the layer 2 ecosystem

- No Immediate Changes

My Ask & Promise on This Proposal

I think that it would be valuable to leave this RFC posted for 2 weeks before moving forward with a temperature check - giving the community sufficient time to weigh several options and provide their thoughts. I will also try to garner community support on what the best Snapshot structure would look like, assuming sufficient support is realized, including what will be specified in the potential outcomes and what type of voting would be preferred.

My ask is to get involvement from large community delegates, including @olimpio , @lefterisjp , @superphiz and @david-mihal before the voting stage. I think it would be very helpful to get their opinions on the proposal during the RFC step, so it may be understood what they are looking for in a proposal as they have a large majority of the active voting power.